For most of us, income is the engine that keeps life running smoothly. It covers everything—from rent or mortgage, to groceries, child care, car payments, and student loans. But what happens if that engine suddenly stalls?

It’s a tough question, but one worth asking:

If you were unable to work due to injury or illness, who would pay your bills?

💵 Your Paycheck Funds Your Life

Most households today rely on every dollar that comes in. Whether you’re single, supporting a family, or working to pay off debt, your paycheck is the foundation of your financial security.

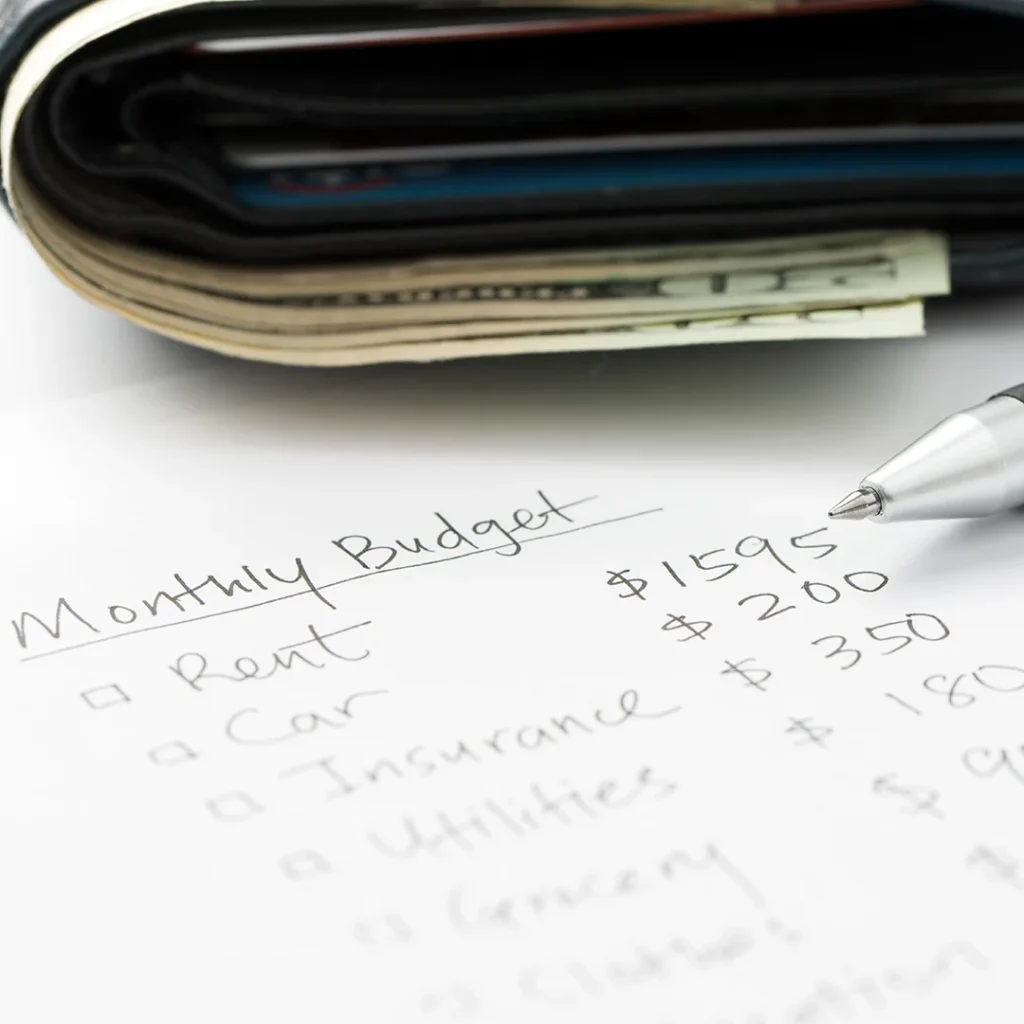

Here are just a few of the monthly essentials your income covers:

- Housing: Rent or mortgage doesn’t stop if you do.

- Childcare & School Costs: Daycare, tuition, clothes, lunches—it all adds up fast.

- Loans & Debt: Student loans, car loans, and credit card payments still expect to be paid, even if you’re out of work.

- Groceries & Utilities: Basic necessities don’t pause when you’re recovering.

Now imagine being out of work for 3, 6, or even 12 months. How far would your savings stretch?

🛡️ Enter Disability Insurance

This is where Disability Insurance becomes a powerful safety net. It helps replace a portion of your income if you’re unable to work due to a covered injury or illness—even if the cause isn’t work-related.

That means you can still pay rent, keep food on the table, cover daycare, and make your loan payments—even while you recover.

It’s not just protection—it’s peace of mind.

👨👩👧👦 Who Needs It?

If any of these sound like you, disability insurance should be on your radar:

- You’re the primary breadwinner

- You support a spouse, kids, or other family members

- You have monthly debt payments

- You rent or own a home

- You’d struggle to cover expenses if your paycheck stopped

In short: if people or payments rely on your income, you can’t afford not to protect it.

✅ Don’t Wait Until It’s Too Late

The reality is that 1 in 4 adults will experience a disability before reaching retirement age (source: Social Security Administration). And most of these are due to illnesses, not accidents.

Disability insurance is often more affordable than people expect—typically just 1–3% of your annual income. That’s a small price for financial security when life doesn’t go as planned.

📩 Get Protected. Stay Prepared.

You work hard to build your life. Don’t leave it vulnerable.

Let’s talk about how disability insurance can help cover the bills—even when you can’t.

👉 Contact us today for more information or to get a personalized quote.

📚 Sources

- Social Security Administration (SSA) – Disability and income protection statistics

- “1 in 4 of today’s 20-year-olds will become disabled before they retire.”

https://www.ssa.gov/disabilityfacts/facts.html

- “1 in 4 of today’s 20-year-olds will become disabled before they retire.”

- Council for Disability Awareness – Common causes and duration of disability

- Most long-term disabilities are caused by illnesses, not accidents.

https://disabilitycanhappen.org/disability-statistic/

- Most long-term disabilities are caused by illnesses, not accidents.

- U.S. Bureau of Labor Statistics (BLS) – Consumer spending and cost of living data

- Details typical household expenses for American families.

https://www.bls.gov/cex/

- Details typical household expenses for American families.

- U.S. News & World Report – Cost of disability insurance

- Disability insurance typically costs 1–3% of your annual income.

https://money.usnews.com/financial-advisors/articles/how-much-does-disability-insurance-cost

- Disability insurance typically costs 1–3% of your annual income.